ESG & Responsible Investment Policy

Q2 2026

Overview

The complete L1 Group ESG & Responsible Investment Charter can be read here.

The L1 Group ESG & Responsible Investment Charter outlines the integrated approach L1 Group and its investment managers take to incorporating environmental, social and governance considerations (“ESG”) into our investment decision-making, our ownership practices and our business operations. It has four key components:

- Responsible investing (RI) and ESG analysis in investment decision-making,

- Active ownership and proxy voting

- Sustainability in our business operations, and

- Modern slavery risk.

Our commitment

L1 Group seeks to provide best-in-class investment products that deliver exceptional risk-adjusted returns for our investors. We are committed to ESG practices because we believe understanding ESG issues can increase long-term returns and better manage risk in our portfolios.

Application

Each investment team in the L1 Group has the discretion and independence to manage assets according to their own investment philosophies and processes.

However, there is a unified commitment to integrating ESG and corporate sustainability into the following L1 Group Strategies and all the pooled vehicles and mandates managed by their investment teams:

- L1 Capital Long Short Team

- L1 Capital International Team

- Platinum Investment Team

The Charter does not cover the strategies managed by the L1 Capital Global Opportunities Team and the L1 Capital U.K. Property Team, each of which adopt their own approaches to investing in accordance with their respective asset classes.

1. Responsible investment

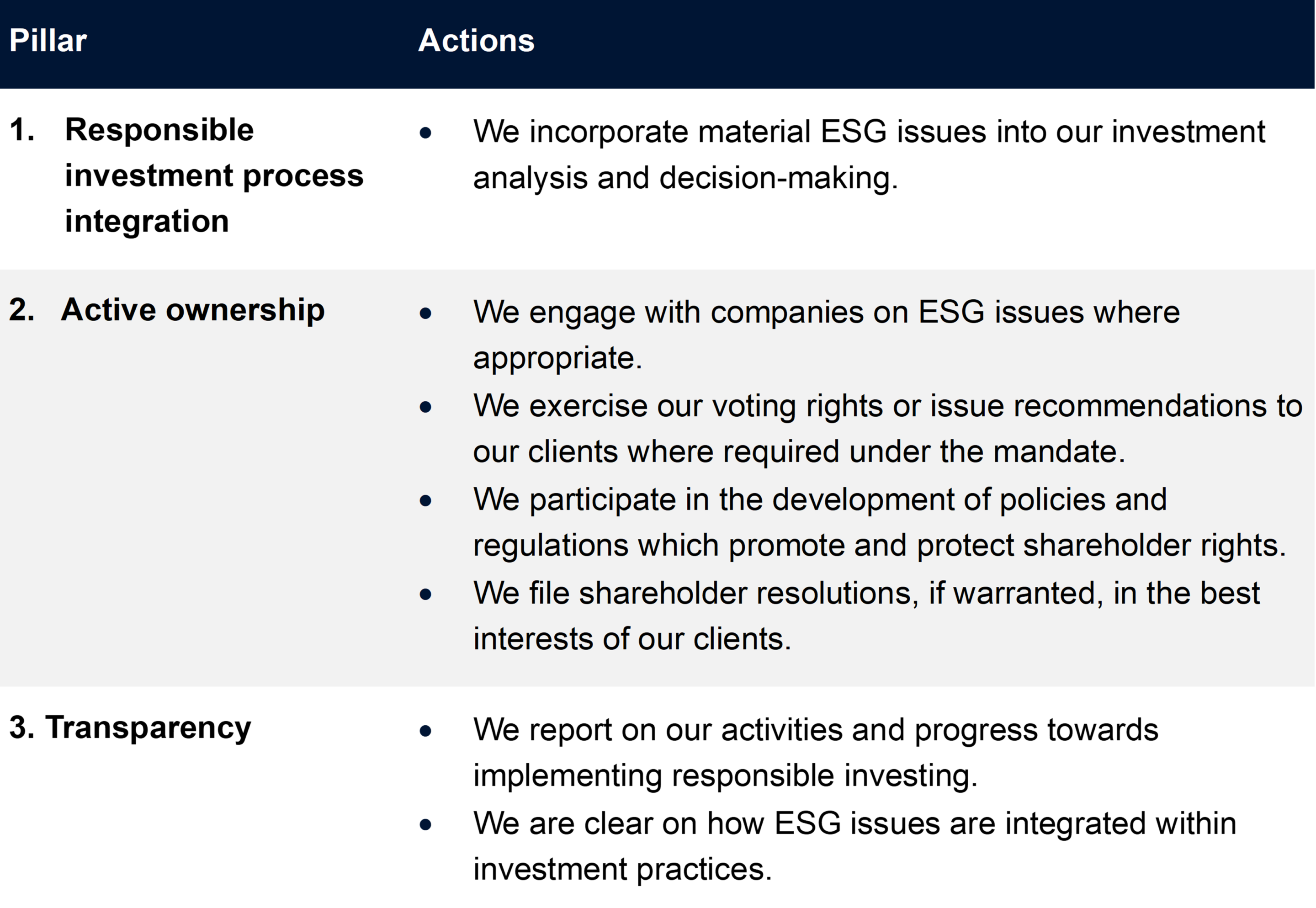

L1 Group’s Pillars

The L1 Group has adopted 3 pillars for Responsible Investing.

ESG analysis in stock analysis

The objective of our RI efforts is to provide a long-term boost to performance for our portfolios. Given the potential implications that ESG issues have on companies’ capital allocation, operating costs, business risks and, therefore, fair value, we believe that we can achieve this objective through cultivating an understanding of material ESG risks and opportunities as we perform our investment research. We do not set ESG objectives that target specific ESG outcomes.

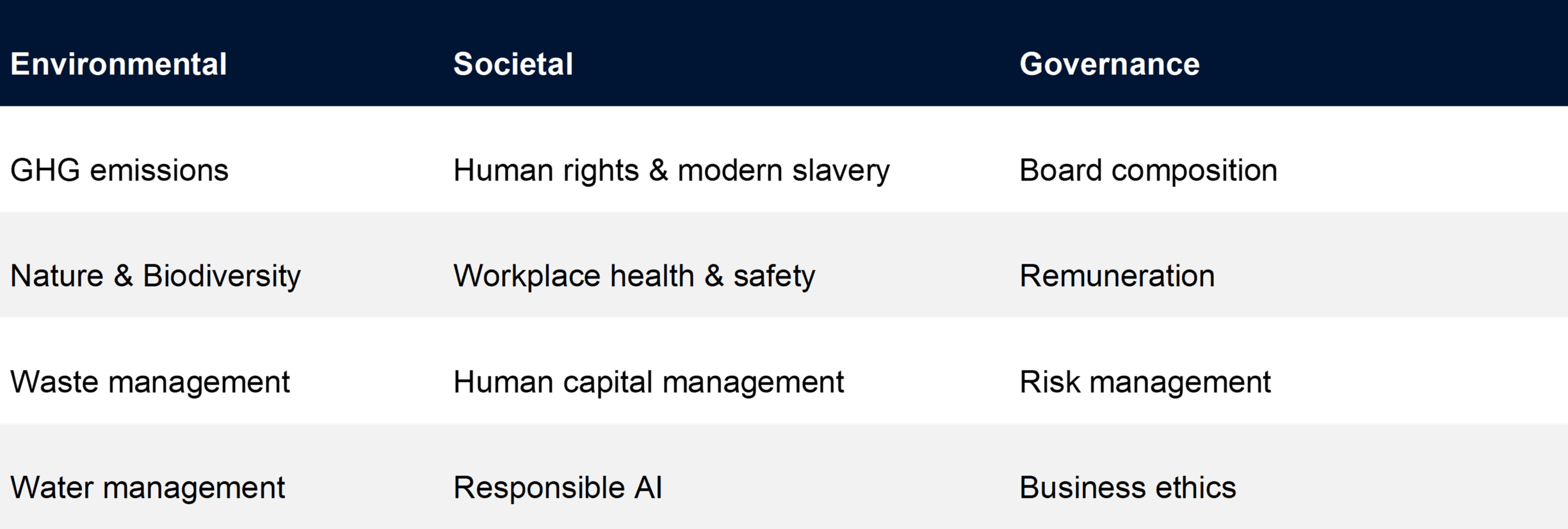

Companies are facing a wide range of issues from an ESG perspective as the regulation and policy settings surrounding these issues continue to evolve. Although L1 Group has no predetermined view about what it regards to be an ESG consideration, some of the material ESG issues we may consider are outlined below.

ESG issues are identified and monitored on an ongoing basis through our fundamental investment research process, supported by a range of external data providers.

L1 Group has no fixed view or methodology for determining how far it will take ESG considerations into account when making investment decisions for a portfolio, other than we will take ESG considerations into account that we may become aware of, but only to the extent such issues impact our view of a company’s inherent value and hence the return on our investment. Consideration of ESG issues provides us with an expanded information set by which we assess the risks and opportunities facing companies.

2. Active ownership and proxy voting

Guiding principles

L1 Group views proxy voting as an important component of our RI approach.

The L1 Group recognises the strong link between good corporate governance and investment outcomes. We believe good governance provides a long-term boost to performance and therefore our efforts to influence corporate governance at the companies we invest in works to improve returns – and reduce risk – in our investment portfolios.

We are active owners and seek to influence policy in the companies we invest in. We do this through discussions with company management and the exercise of voting power.

We believe it is our fiduciary responsibility to exercise our vote on all matters for companies in which our funds are invested where possible. We also engage the services of proxy advisers.

The L1 Group uses its best efforts to vote our proxies, however in some circumstances it may be impractical or not possible to do so.

Conflicts of interest

There may be occasions where L1 Group’s interests conflict, or appear to conflict, with the interests of its clients. L1 Group’s priority is always our clients’ best interests. At no time will we use our proxy voting power to advance our own commercial interests at the expense of our clients’ interests, or to pursue a cause that is unrelated to our clients’ economic best interests.

3. Corporate Sustainability

L1 Group believes the key to the sustainable long-term growth of our business lies in the successful, responsible management of our clients’ money. We are committed to sustainable business practices, including strong governance plus social and environmental awareness.

Corporate governance

L1 Group is committed to maintaining and promoting high standards of corporate governance as we consider this fundamental to the sustainability of our business. L1 Group seeks to promote a culture of risk awareness, accountability and responsiveness. Legal and regulatory compliance is imperative to the success of our business and we expect our directors and staff to act lawfully and ethically at all times. As a public company listed on the Australian Securities Exchange (ASX), our governance arrangements are consistent with the fourth edition of the ASX Corporate Governance Council’s Corporate Governance Principles and Recommendations. For further information, please refer to our Corporate Governance Statement.

Alignment with client interests

L1 Group seeks to act with integrity in all our dealing with clients, intermediaries, business partners, suppliers and regulators. We have implemented robust policies and procedures aimed at preventing unlawful, unethical or improper conduct. Given the nature of our business, we are particularly mindful of the risks of insider trading and ’front running’ and have implemented a range of policies, available here, with which all staff must comply.

L1 Group staff and our Investment teams have large personal investments in our funds, demonstrating a strong, long-term alignment with our investors.

Data privacy and information security

Protecting client data and privacy is of utmost importance to all L1 staff. L1 Group has aligned all its cybersecurity practices to the NIST Cybersecurity Framework (NIST CSF) and invests significant money and effort in continually strengthening its cyber resilience. Cybersecurity is fully integrated into the L1 Group Risk Framework, with regular reporting to the L1 Group Board Audit, Risk & Compliance Committee.

Our Privacy Policy is available here.

Climate change

L1 Group recognises that climate change is a systemic challenge for current and future generations. Extreme weather events and changing weather patterns are impacting on economies and communities around the world. We recognise that corporates and investors must respond to the challenges of climate change and that environmental, social and corporate governance (ESG) issues can affect the performance of our investment portfolios.

We will be reporting in line with the AASB S2 climate-disclosure framework in coming periods.

Diversity equity & inclusion

L1 Group relies on the skill and experience of our people to deliver strong client outcomes. As a result, creating an environment where we can attract, retain and nurture diverse talent is critical to L1 Group’s success. For further information, please refer to our DE&I Policy.

4. Modern slavery risk

L1 Group is committed to addressing modern slavery in our corporate supply chains and investment portfolios in accordance with the requirements of Australia’s Modern Slavery Act 2018 (Cth) (MSA). We report on modern slavery annually via our Modern Slavery Statement which can be viewed here.

Modern slavery statement

The L1 Group implements and enforces effective systems and controls to help to ensure modern slavery is not taking place within its business or supply chains. The L1 Group’s services are provided from its various offices globally. Its directors and employees are subject to a Code of Conduct which sets out high ethical standards for business conduct.

How to assess modern slavery risk

The L1 Group’s primary suppliers include custodians, fund administrators, IT service providers and professional services firms (who typically provide legal, tax, accounting and professional services). The L1 Group has considered its risk profile and that of its primary suppliers. A number of the L1 Group’s large primary suppliers in Australia publish anti-slavery policies and procedures, which the L1 Group has reviewed. Beginning in 2020 we have questioned these suppliers about their anti-modern slavery processes as part of our annual service provider due diligence process.

With certain smaller suppliers where a higher risk of modern slavery is identified, the L1 Group will consider using contract wording (for example, on right to work status and living wage levels over minimum wage figures) to help ensure compliance. This may be reinforced by enhanced annual due diligence of these suppliers.

Modern slavery register

The L1 Group has a Modern Slavery Register to track any incidents of modern slavery. If the L1 Group becomes aware of an incident of modern slavery, it will not attempt to resolve the situation by itself and will ensure its actions are always in the best interests of the suspected victim/s. The L1 Group will consider if further action is required to verify if modern slavery is occurring and whether and how to involve law enforcement. Any response will be appropriate to the circumstances of the situation.